For months, conflicting macroeconomic knowledge have been used to toughen each side of the query about whether or not we’re in a recession.

The great:

The dangerous:

Recession? Inflation? Stagflation? Comfortable or onerous touchdown? Consensus is an increasing number of converging at the view {that a} recession is approaching. The existing questions now are when it’s going to formally hit; how deep and lengthy it’s going to be; and who it’s going to affect maximum. To lend a hand know the way small and medium sized industry (SMB) homeowners and workers are experiencing and perceiving industry and employment, we analyzed behavioral knowledge from greater than two million workers running at multiple hundred thousand SMBs. We additionally carried out a pulse survey in mid-October of 520 homeowners and 1,256 workers to gauge adjustments in sentiment.

Abstract of findings: Homebase high-frequency timesheet knowledge and mid-October proprietor and worker sentiment surveys point out a deceleration in hours labored and workers running, in addition to a dip in proprietor and worker optimism:

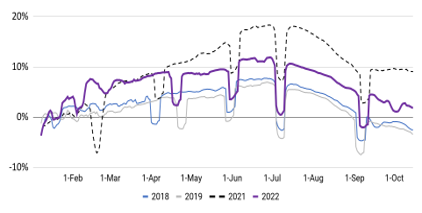

- Our key Major Boulevard Well being Metrics — hours labored and workers running — are down in October vs. September. General hours labored have been down 2.2 percentages issues in October 2022 vs. September 2022. Normally, the fashion in 2022 maximum intently resembles the fashion noticed in 2018 at this level within the yr.

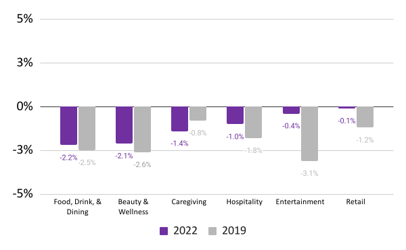

- Maximum {industry} classes exhibited declines in workers running in mid-October vs. mid-September, in line with historic season traits. Main declines have been meals, drink, & eating (-2.2%) and Good looks & Wellness (-2.1%). Leisure (-0.4%) and hospitality (-1.0%) persisted to outperform relative to different industries in 2022, in addition to in comparison with the pre-pandemic length.

- Reasonable (nominal) hourly wages in mid-October remained roughly 13% above figures from January of 2021 and higher modestly month-over-month. Wages proceed to upward thrust. On the other hand, the speed of building up has moderated modestly.

- Sixty-nine p.c of SMB homeowners are positive about how their organizations will most probably carry out this coming Vacation Season. That is very true of the ones homeowners who based their companies after 2020. 40-three p.c of homeowners be expecting the 2022 Vacation Season to be extra winning than it used to be in 2021.

- House owners stay positive, however the development is downwardly biased. Fifty-eight p.c of SMB homeowners imagine that their group can be financially in 365 days relative to lately. This determine represents a month-over-month decline of six proportion issues. A lot of shift happened into the bucket of homeowners who imagine that their group’s financials will appear to be their financials this yr.

Detailed findings

The share of workers running in mid-October used to be down 2.2 proportion issues relative to mid-September. This month-over-month deceleration is in-line with effects from the pre-pandemic length.

Workers running

(Rolling 7-day moderate; relative to Jan. of reported yr)

Major Boulevard Well being Metrics1

(Rolling 7-day moderate; relative to Jan. 2022)

1. Some important dips because of main U.S. vacations. Pronounced dip in mid-February 2021 coincides with the length together with the Texas energy disaster and serious climate within the Midwest. Dip in overdue September coincides with Typhoon Ian. Supply: Homebase knowledge.

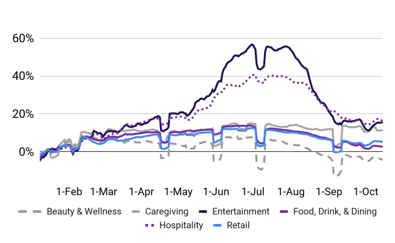

Maximum industries skilled modest month-over-month declines in workers running, in line with seasonal traits.

Context: Save for caregiving, maximum industries have carried out fairly neatly in 2022 with shallower declines than the ones noticed within the corresponding length in 2019.

% trade in workers running

(In comparison to January 2022 baseline the use of 7-day rolling moderate)1

% trade in workers running

(Mid-October vs. mid-September, the use of January 2022 and January 2019 baselines)1

1. October 9-15 vs. Sept. 11-17 (2022) and October 6-12 vs. September 8-14 (2019). Pronounced dips typically coincide with main US Vacations. Supply: Homebase knowledge.

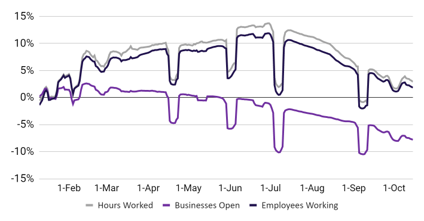

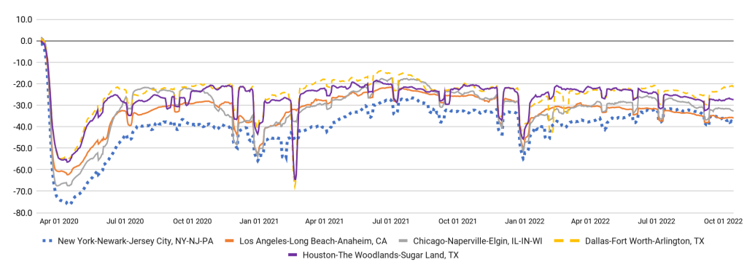

Hours labored within the New York and Los Angeles MSAs reduced modestly in mid-October vs. mid-September. The Houston and Chicago MSAs remained flat month-over-month, and the Dallas MSA higher.

Hours labored

(Rolling 7-day moderate; relative to Jan. 2020 (pre-Covid))

1. Some important dips because of main U.S. vacations. Pronounced dip in mid-February 2021 coincides with the length together with the Texas energy disaster and serious climate within the Midwest. Supply: Homebase knowledge.

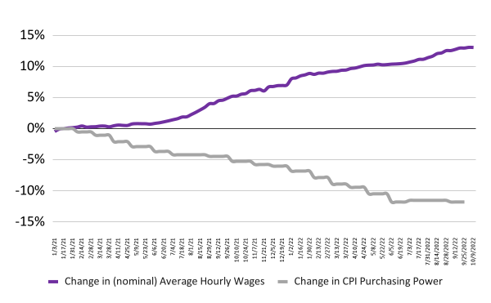

Nominal moderate hourly wages are 13% upper in October of 2022 in comparison to January 2021

Reasonable (nominal) hourly wages are roughly 13% upper in mid-October relative to January 2021. The speed of building up in mid-October used to be in-line with the speed of building up noticed in mid-September.

% trade in nominal moderate hourly wages and CPI Buying Energy of the Shopper Greenback relative to January 2021 baseline1

1. Nominal moderate hourly salary adjustments and the (per month) CPI for all City Shoppers: Buying Energy of the Shopper Greenback in U.S. Towns. Reasonable (non-seasonally adjusted) calculated relative to a January 2021 baseline. Assets: Homebase knowledge, U.S. BLS.

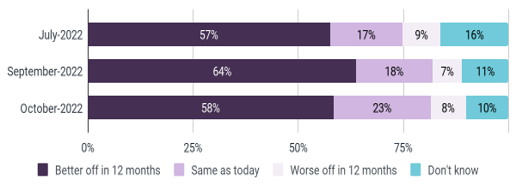

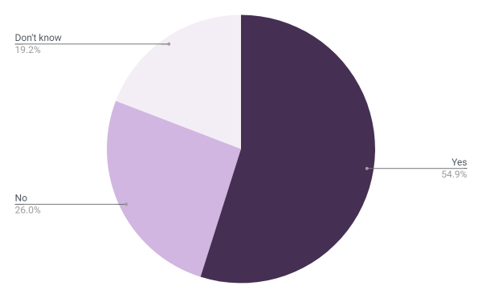

Normally, SMB homeowners stay positive concerning the long run. On the other hand, the relative degree in their optimism declined month-over-month.

Fifty-eight p.c of SMB homeowners imagine that their group can be financially in 365 days relative to lately. This determine represents a month-over-month decline of six proportion issues. A lot of the shift happened into the bucket of homeowners who imagine that their group’s financials subsequent yr will glance the similar as their financials this yr.

House owners of organizations based in 2022 have been essentially the most positive, with 82% believing subsequent yr can be higher for them financially vs. this yr. Organizations based in 2019 or previous have been much more likely to imagine that subsequent yr will both be the similar (48%) or worse (12%) than this yr, with the rest unsure.

Survey query: Do you suppose your company can be , the similar, or worse off financially three hundred and sixty five days from now in comparison to lately?

Supply: Homebase Proprietor Pulse Survey.

Twenty-five p.c of SMB homeowners intend to open new places in their present companies within the subsequent one to 2 years

As of mid-October, 25% of SMB homeowners intend to open new places in their present companies within the subsequent one to 2 years. This determine represents a lower of 4 proportion issues since mid-September and the bottom studying since July 2022.

Survey query: Do you plan to open a brand new location of your present industry within the subsequent 12-14 months?

Supply: Homebase Proprietor Pulse Survey.

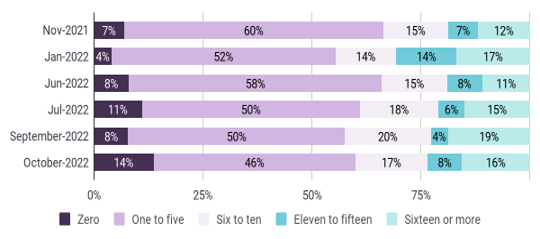

As of October, maximum SMB homeowners supposed to rent further employees within the subsequent 12-24 months

80-six p.c of homeowners plan to rent a number of further employees within the subsequent one to 2 years. Essentially the most incessantly cited vary used to be between one to 5 further employees (46%) adopted via six to 10 further employees (17%).

Even supposing most householders intend to rent further employees, the share of homeowners who now need to make no further hires higher significantly from 8% in September to fourteen% in October, which is the best determine we’ve recorded since we started asking this query in November 2021.

Survey query: What number of further employees do you plan on hiring within the subsequent one to 2 years?

Supply: Homebase Proprietor Pulse Survey.

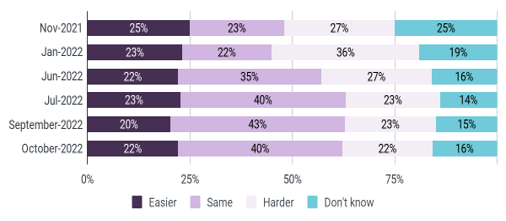

The share of homeowners who imagine it’s going to be more straightforward to rent employees a yr from now higher month-over-month

The vast majority of SMB homeowners intend to rent further workers. We thus requested them whether or not they imagine it’s going to be more straightforward, the similar, or tougher for them to rent employees subsequent yr vs. what they’re experiencing in lately’s exertions marketplace to deduce their perspectives at the path of the exertions marketplace. 40 p.c of homeowners be expecting the exertions marketplace a yr from now to be the similar as it’s lately. Twenty-two p.c of homeowners imagine that it’s going to be more straightforward to rent subsequent yr vs. lately. This determine represents a ten% building up relative to September.

Survey query: Do you suppose it’s going to be more straightforward, the similar, or tougher on your group or industry to rent employees three hundred and sixty five days from now in comparison to lately?

Supply: Homebase Proprietor Pulse Survey.

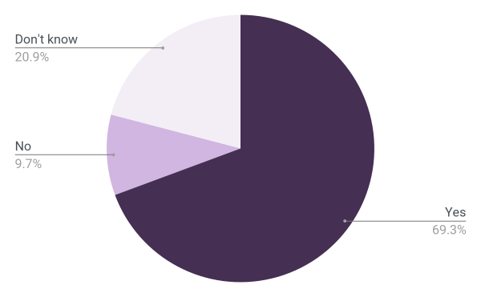

Greater than two-thirds of SMB homeowners are positive about how their organizations will carry out this coming Vacation Season

Sixty-nine p.c of SMB homeowners are positive about how their organizations will most probably carry out this coming Vacation Season.

Survey query: Are you positive about how your company will carry out this Vacation Season?

Supply: Homebase Proprietor Pulse Survey.

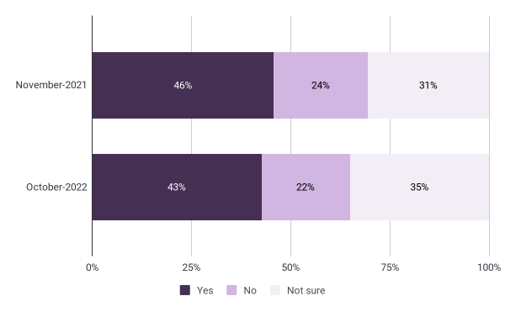

Even supposing homeowners are typically positive concerning the vacations, their expectancies about profitability are down somewhat in 2022 vs. 2021

46% of SMB homeowners anticipated to have a extra winning Vacation Season in 2021 vs. 2020. In October of 2022, 43% of SMB homeowners be expecting to have a extra winning Vacation Season vs. the prior yr.

This decline in optimism may also be attributed to an building up in uncertainty as 35% of SMB homeowners don’t seem to be positive whether or not Vacation Season 2022 can be extra winning than in 2021 when 31% expressed uncertainty about organizational profitability relative to the prior (Covid) yr.

Survey query: Do you are expecting to have a extra winning Vacation Season this yr in comparison with closing yr?

Supply: Homebase Proprietor Pulse Survey.

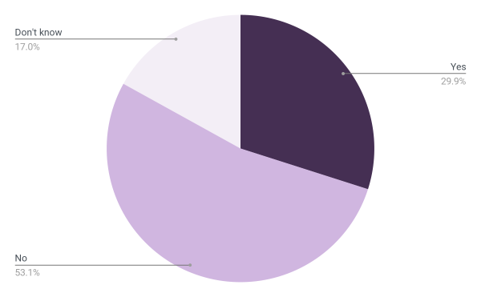

So far, most householders haven’t begun to look a upward thrust in buyer task associated with the Vacation Season

We requested SMB homeowners whether or not they’ve noticed a upward thrust in buyer task in anticipation of the 2022 Vacation Season. As of mid-October, kind of 30% of homeowners have noticed an uptick in buyer task while the bulk have no longer.

Some information resources have reported that vacation gross sales will get started previous this yr. We requested SMB homeowners whether or not they supposed to do likewise.

- Early gross sales: Twenty-nine p.c of homeowners are making plans on providing vacation promotions previous; fifty p.c file no longer doing so, and the rest are undecided of whether or not they’ll be offering previous reductions to lure consumers.

- Reductions to offset inflation: Thirty p.c of SMB homeowners plan to provide reductions to lend a hand consumers cope with inflationary pressures; 52% don’t seem to be making plans on providing reductions and 18% are undecided if they’ll accomplish that.

Survey query: So far, have you ever noticed a upward thrust in buyer task associated with the Vacation Season (e.g., extra visitors, more potent gross sales)?

Supply: Homebase Proprietor Pulse Survey.

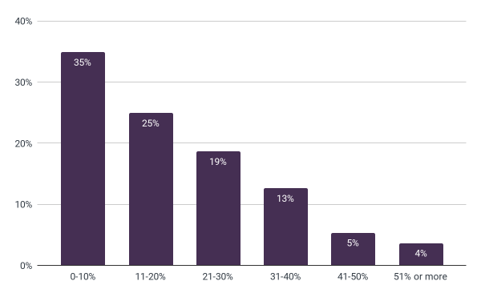

For forty-one p.c of homeowners, the vacation season contributes greater than twenty p.c of once a year earnings

For 35% of SMBs, the Vacation Season contributes ten p.c or much less of general once a year earnings. 1 / 4 of SMBs derive between 11-20% of once a year earnings all over the Vacation Season. For the remainder forty-one p.c of homeowners, the Vacation Season in an ordinary yr is when greater than twenty p.c of once a year source of revenue is generated.

- What month is busiest for vacation gross sales? We requested homeowners what month they anticipated to be the busiest for his or her vacation gross sales. The reaction used to be overwhelming: 65% indicated it might be December, adopted via November (29%), and October (6%).

Survey query: How a lot of your once a year earnings is made all over the Vacation Season in an ordinary yr?

Supply: Homebase Proprietor Pulse Survey.

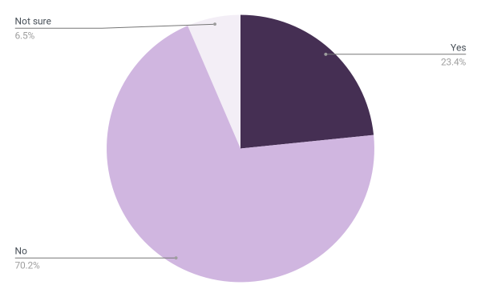

SMB homeowners face a number of demanding situations. On the other hand, hiring sufficient seasonal employees isn’t a question this is regarding homeowners at this time

Just a fairly small proportion of homeowners (23%) are interested by discovering sufficient employees to hide their vacation staffing wishes.

On moderate, homeowners be expecting to enlarge their worker bases via eighteen p.c for the vacations.

Most likely on account of those perspectives about exertions wishes, 31% of homeowners plan on paying workers extra all over the vacation season; 53% don’t; and 17% are undecided.

Survey query: Are you interested by discovering sufficient employees to hide your vacation staffing wishes?

Supply: Homebase Proprietor Pulse Survey.

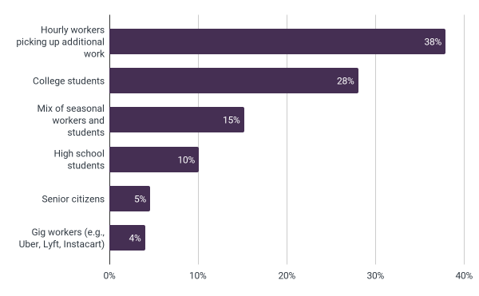

When on the lookout for seasonal employees, SMB homeowners get the most productive effects with hourly employees on the lookout for further shifts adopted via school scholars

Hiring for the vacations–or any brief period–includes further demanding situations as a result of the want to get employees temporarily up to the mark. We thus requested SMB homeowners the place, in accordance with their revel in, they in finding the most productive seasonal employees. The #1 reaction used to be hourly employees having a look to select up further paintings, cited via 38% of SMB homeowners. The second one maximum incessantly cited reaction used to be school scholars (28%). Gig-workers have a tendency to price fairly low (4%), then again.

Survey query: In response to your revel in, which of the next forms of employees make the most productive seasonal employees for your enterprise?

Supply: Homebase Proprietor Pulse Survey.

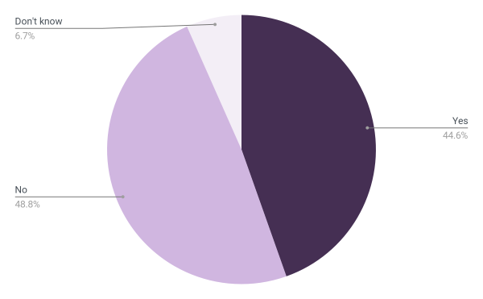

Just about forty-five p.c of homeowners are experiencing difficulties acquiring fundamental fabrics or elements–basically because of price will increase or shortages

The main causes cited for difficulties acquiring fundamental fabrics or elements have been:

- Product shortages (74%)

- Value will increase in intermediate items (62%)

- Longer delivery occasions (52%)

- Some aggregate of these types of components (5%)

Survey query: Are you having a harder time acquiring subject matter/elements you wish to have?

Supply: Homebase Proprietor Pulse Survey.

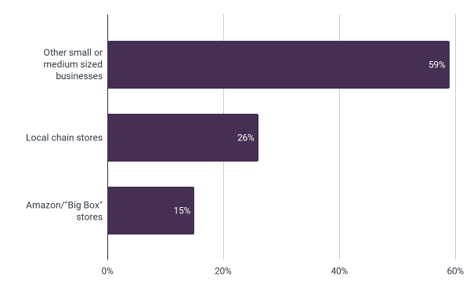

Maximum SMBs view different SMBs or native chains as their largest competition

Opposite to traditional knowledge that makes a speciality of the affect of enormous companies on “native” industry alternatives, SMB homeowners basically view different SMB companies as their largest competition (59%), adopted via native chain shops (26%) and, in the end, huge shops or Amazon or different industry-relevant “Large Field” shops.

The image is, alternatively, extra nuanced for the ones SMBs in retail or client items. For those companies, different SMBs have been nonetheless the most important competition (41%). On the other hand, the distance between native chains (30%) and Amazon/“Large field” shops (29%) narrowed.

Survey query: Who’s your largest competitor?

Supply: Homebase Proprietor Pulse Survey.

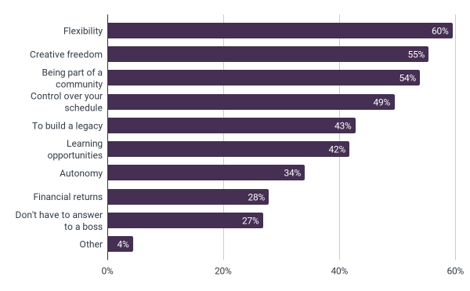

What are SMB homeowners’ favourite facets of proudly owning a industry? (Trace: It isn’t the cash.)

Trade possession is a cornerstone of the “American Dream.” SMBs also are a key motive force of the United States economic system and exertions pressure. We thus requested SMB homeowners what they favored maximum about proudly owning a industry.

Curiously, SMB homeowners don’t seem to be (basically) in it for the cash (28%), loss of a md to reply to to (27%), or for the autonomy it will possibly have enough money (34%). Relatively, essentially the most incessantly cited “favourite” sides of proudly owning an SMB come with flexibility (60%), adopted intently via ingenious freedom (55%), being a part of a group (54%), and keep an eye on over one’s time table (49%).

Survey query: What are your favourite portions of proudly owning a small industry (take a look at all that observe)?

Supply: Homebase Proprietor Pulse Survey.

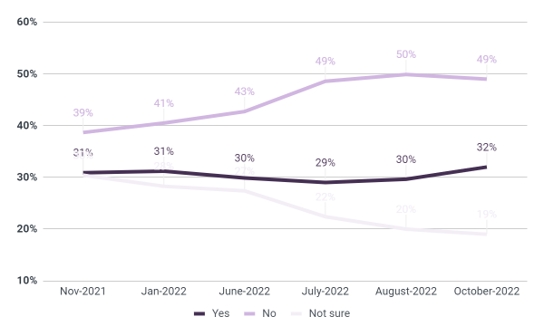

In keeping with effects from July and August, typically, workers don’t intend to search for a brand new process

Since July of 2022, the share of workers who do no longer intend to search for a brand new process within the subsequent one to 2 years has remained above roughly 49% (achieving a near-term excessive of just about 50% in August).

Survey query: Do you plan to search for a brand new process within the subsequent 12-24 months?

Supply: Homebase Worker Pulse Surveys.

Maximum workers be expecting to paintings extra shifts this vacation season, and a few 3rd have noticed extra alternatives for seasonal paintings this yr

Maximum workers (54%) be expecting to paintings extra shifts all over the Vacation Season.

When put next with this time closing yr, 32% of workers have noticed extra alternatives for seasonal paintings, 33% have no longer, and the rest are unsure at this level.

Survey query: Do you are expecting to paintings extra shifts this Vacation Season?

Supply: Homebase Worker Pulse Surveys.

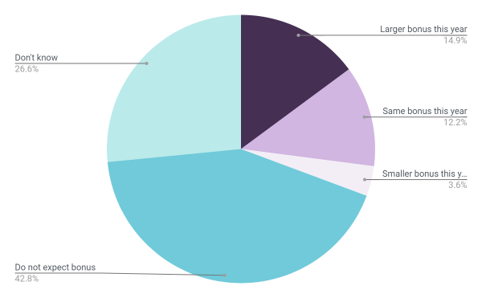

Bah humbug: 43% of workers don’t be expecting to obtain a vacation bonus this yr

43% of workers don’t be expecting to obtain a vacation bonus this yr and 27% are unsure whether or not they’ll or won’t obtain a vacation bonus. For the ones workers who be expecting to obtain an advantage, a somewhat upper proportion (14.9%) be expecting to obtain a bigger bonus than closing yr vs. those that be expecting to obtain the same quantity as closing yr (12.2%).

Even supposing a excessive proportion of workers don’t be expecting to obtain a vacation bonus this yr, a better proportion of workers really feel extra valued via their employers (35%) vs no longer (32%) all over the vacations.

Survey query: Do you are expecting to obtain a bigger, the similar, or a smaller vacation bonus this yr vs. closing yr?

Supply: Homebase Worker Pulse Surveys.

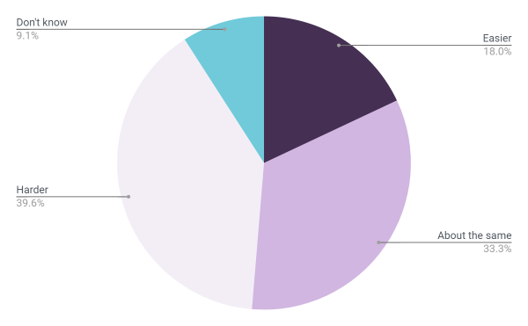

Workers be expecting it to be tougher to have enough money items this yr vs. closing yr

Roughly 40 p.c of workers imagine that it’s going to be tougher to have enough money items this yr vs. closing yr; a few 3rd imagine it’s going to be about the similar and handiest eighteen p.c suppose it’s going to be more straightforward.

Survey query: Do you suppose it’s going to be more straightforward, about the similar, or tougher to have enough money the items you hope to buy this yr vs. closing yr?

Supply: Homebase Worker Pulse Surveys.

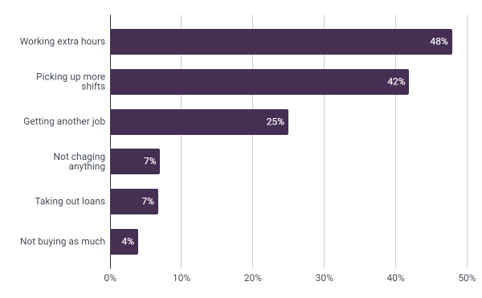

And not using a vacation bonus and better present prices, workers are running additional hours, selecting up extra shifts, or discovering further paintings

With a excessive proportion of workers no longer anticipating a vacation bonus and a in a similar way excessive proportion anticipating items to be much less inexpensive this yr vs. closing yr, workers are running additional hours (48%), selecting up extra shifts (42%), or getting any other process (25%) to have enough money vacation items.

Survey query: Are you doing any of the next to have enough money vacation items this season (take a look at all that observe)?

Supply: Homebase Worker Pulse Surveys.

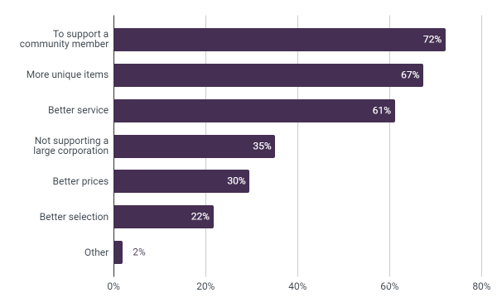

As shoppers, SMB workers store “small” to toughen group participants, for distinctive pieces, and for higher carrier

SMB workers also are shoppers. As we consider the Vacation Season, we requested SMB homeowners what the advantages of buying groceries at a small industry are. The #1 reason why they cited used to be to toughen a group member (72%), extra distinctive pieces (67%), or higher carrier (61%)—suggesting those are all components small companies can emphasize to compete with huge firms. Curiously, 35% additionally store at small companies in order that they’re no longer supporting a big company. As one worker:

“Small companies are superb as a result of there’s extra care put into the paintings and merchandise you purchase.”

Survey query: What are the advantages of buying groceries at a small industry (take a look at all that observe)?

Supply: Homebase Worker Pulse Surveys.

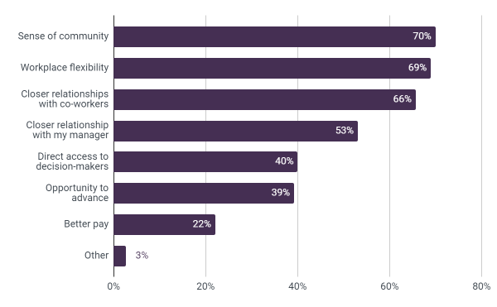

SMB workers are drawn to paintings at small companies for a way of group, flexibility, and relationships

SMB workers’ choice for group is a key motive force in their enchantment to paintings at a small vs. huge industry (70%). Like SMB homeowners, SMB workers additionally extremely price flexibility (69%).

In keeping with the emphasis of group, SMB workers additionally extremely price relationships, with 66% bringing up shut relationships with co-workers as a reason why they have been drawn to paintings at a small vs. huge industry, and 53% bringing up a better dating with their managers.

Survey query: What draws you to paintings at a small industry vs. a big industry (take a look at all that observe)?

Supply: Homebase Worker Pulse Surveys.